NBCC (India) Limited, trading at ₹109.25 as of July 2025, presents a compelling investment case with analyst price targets ranging from ₹125 to ₹223 for 2025. The government-owned construction and infrastructure giant has demonstrated robust financial performance with consistent revenue growth and strong order book visibility, making it an attractive option for investors seeking exposure to India’s infrastructure boom.

Current Market Position and Valuation

NBCC (India) Limited, listed on NSE with symbol NBCC and BSE code 534309, currently commands a market capitalization of ₹30,693 crores. The stock has experienced significant volatility with a 52-week range of ₹70.80 to ₹139.83, reflecting both market uncertainty and growth potential.

The company’s current valuation metrics indicate a premium positioning with a P/E ratio of 56.72x and P/B ratio of 12.38x. While these multiples appear elevated compared to traditional value metrics, they reflect the market’s confidence in NBCC’s growth trajectory and its strategic position in India’s infrastructure development.

Key Financial Metrics Analysis

NBCC’s financial health remains robust with ROE of 23.01% and ROCE of 26.74%, indicating efficient capital utilization and strong returns for shareholders. The company maintains a dividend yield of 0.59% with minimal debt, as evidenced by its near-zero debt-to-equity ratio. The EPS of ₹2.00 reflects consistent profitability despite the cyclical nature of the construction industry.

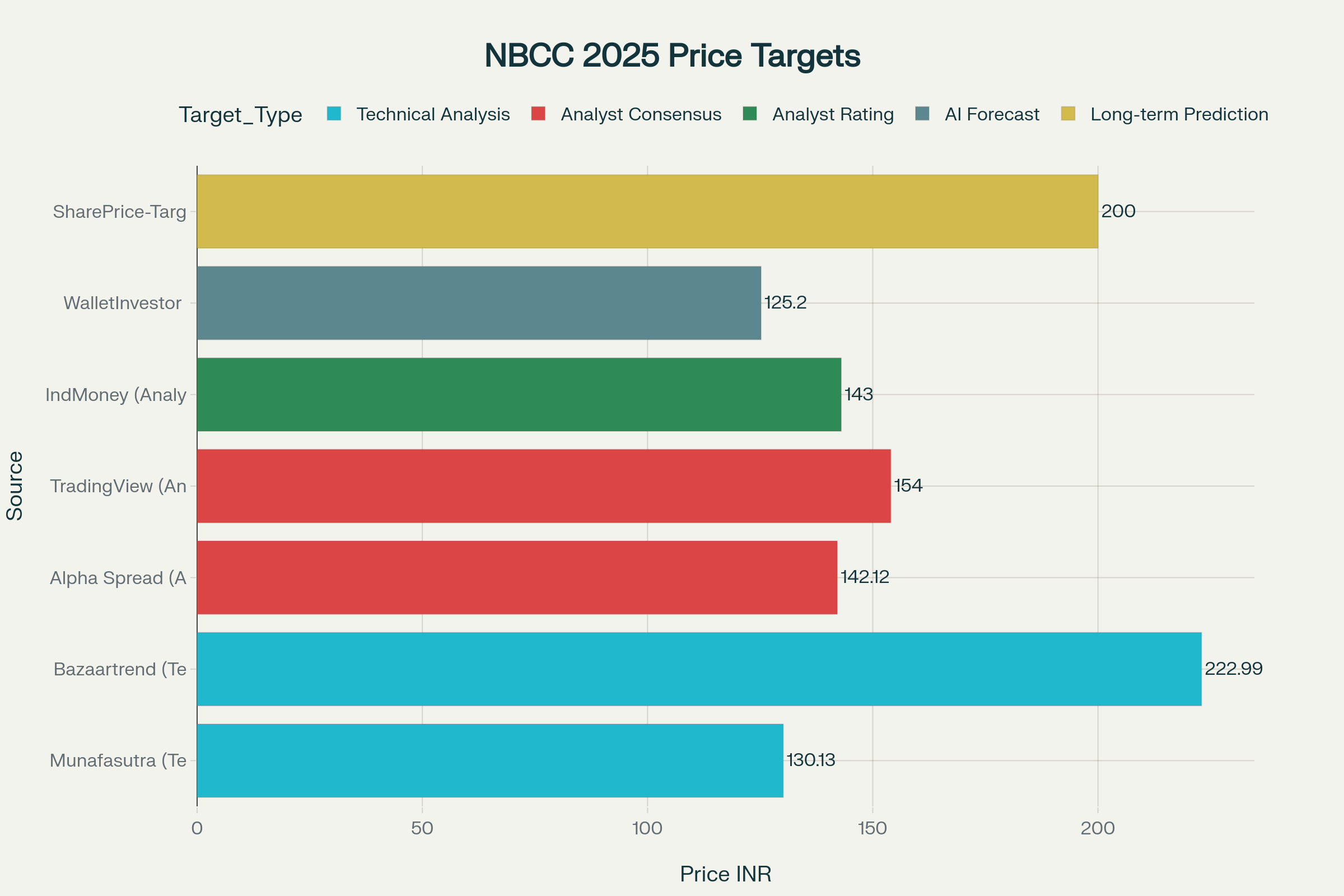

NBCC Share Price Targets 2025 from Various Sources

NBCC Share Price Target 2025: Analyst Consensus and Forecasts

Multiple research houses and analytical platforms have provided varied ** reflecting different methodologies and market perspectives. The consensus among analysts suggests upside potential of 15-30% from current levels.

- Alpha Spread’s analyst consensus places the average 1-year price target at ₹142.12 with a range between ₹111.1 and ₹173.25. This represents approximately 30% upside from current trading levels, driven by expected revenue growth and margin expansion.

- TradingView analysts have set a more optimistic target of ₹154.00, with estimates ranging from ₹143 to ₹165. This higher target reflects confidence in NBCC’s execution capabilities and the strong government infrastructure spending pipeline.

- IndMoney’s analyst rating suggests a target price of ₹143.00, representing a 25.79% upside potential. This conservative yet positive outlook aligns with the company’s steady financial performance and order book visibility.

- Technical analysis from Munafasutra indicates multiple resistance levels, with the highest target at ₹130.13 based on chart patterns and momentum indicators. Bazaartrend’s technical analysis provides more aggressive targets up to ₹222.99, though these appear optimistic given current market conditions.

- Long-term forecasting models, including WalletInvestor’s AI-driven predictions, suggest a more conservative approach with December 2025 targets around ₹125.20. These models factor in market volatility and sector-specific risks while maintaining a positive outlook.

Financial Performance Analysis

NBCC’s recent financial performance demonstrates consistent growth trajectory with strengthening fundamentals. The company’s FY2025 performance showcased remarkable resilience and execution capabilities despite challenging market conditions.

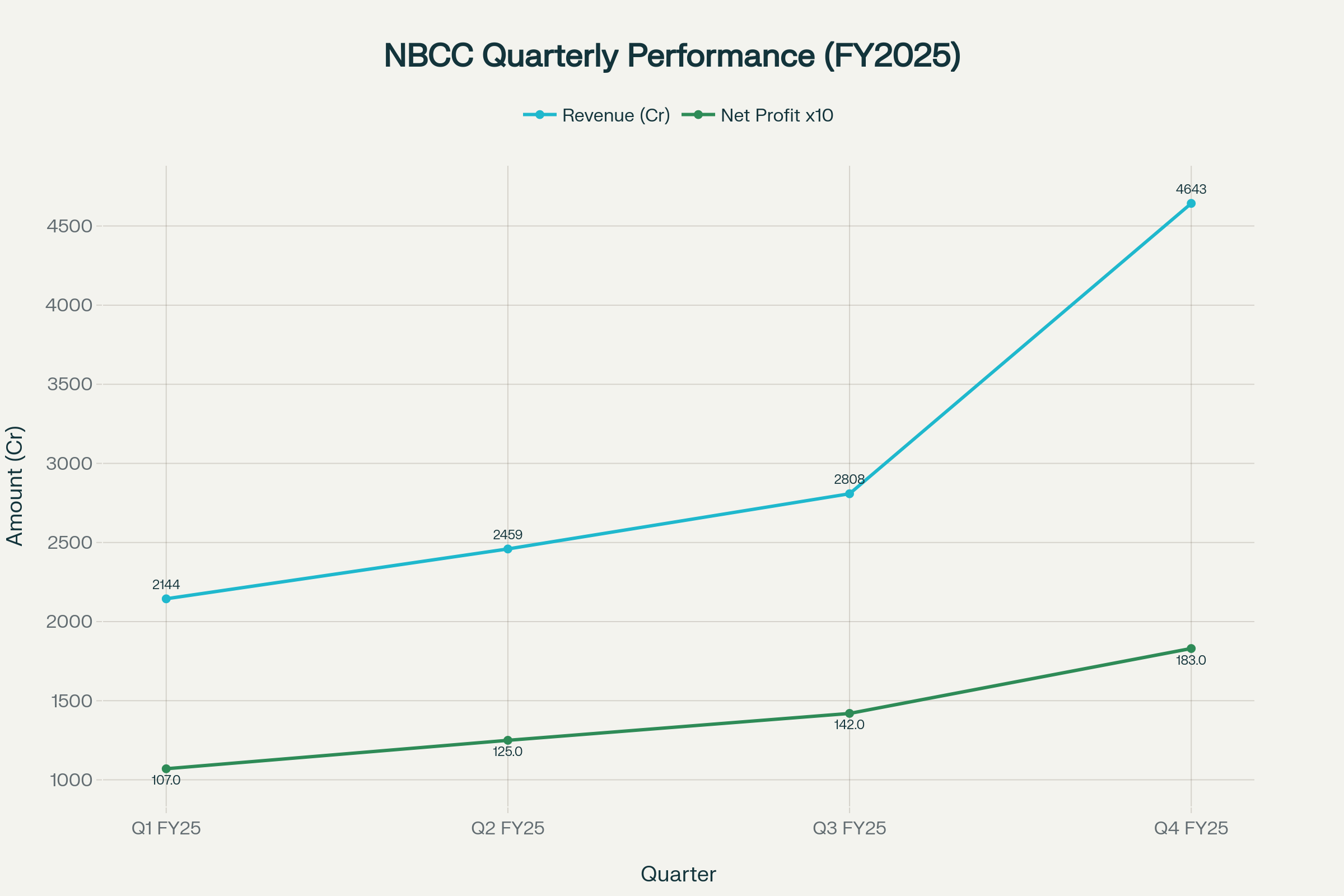

Quarterly Performance Trends

The company’s quarterly results for FY2025 reveal accelerating revenue growth and improving profitability margins. Q4 FY2025 revenue reached ₹4,643 crores, marking a 64.22% quarter-on-quarter increase and 16.17% year-on-year growth. This exceptional performance was driven by project execution acceleration and new order completions.

Net profit margins showed consistent improvement throughout FY2025, with Q4 delivering ₹183 crores in net profit, representing a 28.67% quarter-on-quarter increase and 29.45% year-on-year growth. The EPS progression from ₹0.39 in Q1 to ₹0.65 in Q4 demonstrates the company’s ability to translate revenue growth into shareholder value.

NBCC Quarterly Financial Performance Trend in FY2025

Operating margins expanded to 6.25% in Q4 FY2025, up from 5.04% in the previous quarter, indicating improved project profitability and operational efficiency. This margin improvement reflects better project selection, cost management, and economies of scale.

Annual Financial Highlights

For the full financial year FY2025, NBCC achieved consolidated revenue of ₹12,039 crores, representing a 15.68% increase from FY2024. The company’s total income growth of 15% was complemented by net profit growth of 35%, showcasing operational leverage and improved execution capabilities.

EBITDA margins improved to approximately 5.5-6% as guided by management, with Chairman and MD K P Mahadevaswamy indicating stable margin trajectory for FY2026. The company maintains a strong balance sheet with minimal debt and robust cash flows from operations.

Business Segments and Revenue Drivers

NBCC operates through three primary business segments, each contributing to its diversified revenue stream and growth potential. Understanding these segments is crucial for evaluating the NBCC share price target 2025 and long-term investment prospects.

Project Management Consultancy (PMC)

The PMC segment remains NBCC’s largest revenue contributor, accounting for approximately 93% of total business. This segment involves providing comprehensive project management services for government infrastructure projects, including planning, design supervision, and project execution oversight.

Recent major PMC wins include the ₹296.53 crore Meerut Development Authority project secured in June 2025, demonstrating continued government confidence in NBCC’s execution capabilities. The company’s established relationships with various government departments and agencies provide a steady pipeline of PMC opportunities.

Engineering Procurement & Construction (EPC)

The EPC segment contributes approximately 4% of total business but offers significant growth potential. NBCC undertakes turnkey construction projects, including power sector infrastructure like chimneys and cooling towers. This segment benefits from India’s expanding industrial and energy infrastructure requirements.

Recent developments in the EPC segment include strategic partnerships and capability expansion to handle larger and more complex projects. The segment’s growth trajectory aligns with India’s infrastructure development goals and industrial expansion plans.

Real Estate Development

Real Estate Development accounts for 3% of total business but represents substantial value creation potential. NBCC develops residential and commercial properties for government departments and agencies, with recent success including the ₹1,467.93 crore sale of 446 residential units at Aspire Silicon City, Noida.

The real estate segment benefits from urbanization trends and government housing initiatives like Pradhan Mantri Awas Yojana. NBCC’s strategic land bank and development expertise position it well for future real estate opportunities.

Recent Developments and Order Book Analysis

NBCC’s robust order book provides strong revenue visibility supporting the positive NBCC share price target 2025 outlook. The company’s systematic approach to order acquisition and execution has resulted in a healthy project pipeline.

Major Order Wins in 2025

- March 2025 marked a significant milestone with NBCC signing a ₹25,000 crore MoU with MAHAPREIT (Mahatma Phule Renewable Energy and Infrastructure Technology Limited) for Maharashtra infrastructure projects. This strategic partnership covers cluster development, data centers, renewable energy initiatives, and slum rehabilitation projects across Maharashtra.

- June 2025 saw NBCC securing the ₹296.53 crore redevelopment project from Meerut Development Authority, further strengthening its presence in Uttar Pradesh’s urban development sector. This project involves comprehensive redevelopment services under the PMC model.

- April 2025 brought multiple smaller contracts totaling ₹64.67 crores across educational infrastructure projects in Delhi, Hyderabad, and Odisha. These projects demonstrate NBCC’s diversified client base and expertise across different infrastructure segments.

Order Book Composition and Execution Timeline

The company’s aggregate order book stands at approximately 3.5 times its operating income, providing strong revenue visibility for the next 2-3 years. This healthy order book-to-revenue ratio supports analysts’ confidence in achieving NBCC share price targets for 2025.

Project execution timelines have improved significantly, with management focusing on milestone-based delivery and efficient resource allocation. The company’s 31 regional offices across India enable decentralized execution and closer client relationships.

Industry Outlook and Growth Drivers

India’s construction industry presents a favorable backdrop for NBCC’s growth, with multiple structural drivers supporting long-term expansion. Understanding these industry dynamics is essential for evaluating NBCC share price target 2025 projections.

India Construction Industry Growth Trajectory

GlobalData expects India’s construction industry to grow by 7.1% in real terms in 2025, driven by public and private sector investments in energy, industrial, and railway projects. The government’s plan to expand nuclear capacity from 8.9GW in 2024 to 100GW by 2047 creates substantial infrastructure opportunities.

The FY2025-26 Budget outlines total expenditure of INR50.7 trillion ($603 billion), with major allocations including INR2.9 trillion for Ministry of Road Transport and Highways and INR2.6 trillion for Ministry of Railways. These allocations directly benefit NBCC’s core business segments.

Construction market valuation is projected to reach INR 25.31 trillion by 2025, marking an annual growth rate of 11.2%. The sector’s CAGR of 8.8% from 2025 to 2029 positions it among India’s fastest-growing industries.

Government Infrastructure Push

The Ministry of Rural Development’s Pradhan Mantri Awaas Yojana-Gramin (PMAY-G) plans to construct 49.5 million homes by March 2029, creating massive opportunities for construction companies like NBCC. This ambitious housing program aligns perfectly with NBCC’s expertise in residential development.

Smart Cities Mission and various urban development initiatives provide additional growth avenues for NBCC’s PMC and EPC segments. The company’s established government relationships position it advantageously for these large-scale projects.

Nuclear power expansion presents specialized opportunities, with eight nuclear reactors totaling 6.6GW capacity under construction as of April 2025. NBCC’s technical capabilities and security clearances make it eligible for such strategic projects.

Risk Factors and Challenges

While the NBCC share price target 2025 outlook remains positive, several risk factors warrant careful consideration by investors. Understanding these challenges is crucial for making informed investment decisions.

Operational and Market Risks

High customer concentration risk poses a significant challenge, with approximately 85% of NBCC’s revenue derived from government contracts. This heavy reliance on public sector projects creates vulnerability to policy changes, budget allocations, and political cycles.

Regulatory compliance costs have increased by 15% in FY2023 due to stricter environmental and safety requirements. These escalating compliance costs can impact project margins and overall profitability.

Supply chain disruptions resulted in project backlogs worth over ₹1,000 crores in Q2 FY2023, highlighting operational vulnerabilities. Material cost inflation averaging 6.5% in 2023 creates additional margin pressure.

Financial and Strategic Risks

Project execution delays remain a persistent challenge in the construction industry, with average cost overruns of 10% reported in recent contracts. These delays can impact cash flows and client relationships.

Currency exposure from international projects poses financial risks, particularly with the rupee depreciation to ₹82 per USD affecting overseas project costs. NBCC’s international operations, while limited, remain exposed to foreign exchange volatility.

Increased competition from major players like Larsen & Toubro, DLF Limited, and Hindustan Construction Company intensifies bidding wars and margin pressure. New entrants offering 5-10% lower bids than established players create additional competitive challenges.

Valuation and Market Risks

Multiple valuation models suggest NBCC may be overvalued at current levels. Peter Lynch’s Fair Value model indicates a fair value of ₹50.10, suggesting the stock is overvalued by 55.92% at current prices. Smart-Investing’s analysis shows an intrinsic value of ₹59.56, indicating 84% premium to estimated fair value.

High P/E and P/B ratios of 56.72x and 12.38x respectively suggest expensive valuation compared to historical averages and sector peers. This premium valuation increases sensitivity to any disappointment in financial performance or order wins.

Peer Comparison and Competitive Analysis

NBCC’s competitive positioning within India’s construction and infrastructure sector provides important context for evaluating share price targets for 2025. Comparing key metrics with industry peers reveals relative strengths and weaknesses.

Key Peer Comparison Metrics

Larsen & Toubro (L&T), the sector leader, trades at a P/E of 40.95x with a market capitalization of ₹4,76,596 crores. L&T’s lower P/E ratio despite its market leadership suggests NBCC’s premium valuation relative to fundamentals.

Rail Vikas Nigam (RVNL) exhibits a P/E of 65.32x with market cap of ₹77,625 crores, indicating that infrastructure PSUs generally trade at premium valuations. NBCC’s P/E of 56.72x appears reasonable within this peer group context.

IRB Infrastructure trades at a more reasonable P/E of 29.69x with market cap of ₹29,223 crores, though its focus on toll roads differs from NBCC’s diversified portfolio. KEC International shows a P/E of 71.98x with market cap of ₹23,107 crores, indicating varied valuation premiums across the sector.

Relative Financial Performance

NBCC’s ROE of 23.01% compares favorably with sector averages, demonstrating efficient equity utilization. The company’s ROCE of 26.74% indicates superior capital efficiency compared to many infrastructure peers.

Revenue growth rates for NBCC have consistently outpaced several peers, with 15.68% YoY growth in FY2025 demonstrating strong execution capabilities. However, absolute revenue size remains significantly smaller than major players like L&T.

Order book quality and government relationships provide NBCC with competitive advantages, particularly in PMC services where relationships and track record are crucial. The company’s Navratna status enhances its credibility for large government projects.

Technical Analysis and Chart Patterns

Technical analysis provides additional insights into NBCC share price target 2025 projections, complementing fundamental analysis with market sentiment and price action indicators.

Key Technical Levels and Targets

Munafasutra’s technical analysis identifies multiple resistance and support levels for NBCC. Immediate resistance lies at ₹113.71, ₹115.61, and ₹118.30, while the ultimate technical target reaches ₹130.13. These levels represent significant price action zones where institutional activity has historically occurred.

Support levels are identified at ₹88.89, ₹98.77, providing downside protection in case of market corrections. The stock’s current trading around ₹109.25 sits between these key technical levels.

Bazaartrend’s analysis suggests more aggressive upside targets, with the 4th UP Target at ₹222.99 for July 2025. While these targets appear optimistic, they reflect bullish technical momentum and chart patterns.

Moving Average Analysis

50-day and 200-day moving averages provide trend direction insights. NBCC’s price above both moving averages indicates bullish technical positioning supporting positive price targets. The EMA analysis shows the stock trading above short, medium, and long-term exponential moving averages.

RSI indicators suggest the stock is neither overbought nor oversold, providing room for further upward movement toward target prices. MACD signals and other momentum indicators support the bullish technical outlook.

Investment Recommendations and Outlook

Based on comprehensive analysis of fundamentals, industry outlook, and technical factors, NBCC presents a mixed investment proposition for 2025. The positive share price targets are supported by strong business fundamentals and industry tailwinds, but elevated valuations warrant caution.

Investment Positives

Strong order book visibility provides revenue predictability for the next 2-3 years, supporting analyst confidence in growth projections. The company’s established government relationships and Navratna status create competitive moats in the PMC segment.

India’s infrastructure boom driven by government spending and urbanization creates substantial long-term opportunities for NBCC. The company’s diversified business model across PMC, EPC, and real estate reduces sector-specific risks.

Improving financial metrics including margin expansion and profit growth demonstrate operational efficiency gains. Minimal debt levels provide financial flexibility for growth investments and acquisitions.

Investment Cautions

Premium valuation multiples suggest limited margin of safety at current price levels, with intrinsic value estimates significantly below market price. High government dependency creates vulnerability to policy changes and budget constraints.

Intense competition and margin pressure from aggressive bidding could impact future profitability. Execution risks inherent in large infrastructure projects pose operational challenges.

Target Price Synthesis and Recommendation

Synthesizing various analyst targets and valuation methodologies suggests a realistic NBCC share price target range of ₹125-145 for 2025, representing 15-30% upside potential from current levels. This range balances optimistic growth projections with valuation concerns.

Conservative investors might consider the lower end of this range around ₹125-130, while growth-oriented investors could target the higher range of ₹140-145. The wide target range reflects uncertainty in market conditions and execution risks.

Long-term investors with 3-5 year horizons may find NBCC attractive despite near-term valuation concerns, given India’s infrastructure development trajectory and NBCC’s strategic positioning. Short-term traders should monitor technical levels and government project announcements for entry and exit timing.

Conclusion

NBCC share price target 2025 analysis reveals a company well-positioned to benefit from India’s infrastructure expansion, though current valuations suggest measured expectations are appropriate. The consensus target range of ₹125-145 represents reasonable upside potential while acknowledging valuation and execution risks.

Key investment merits include strong government relationships, healthy order book, improving margins, and exposure to India’s infrastructure theme. Primary concerns center on premium valuations, government dependency, and competitive pressures.

Investors should approach NBCC with a balanced perspective, recognizing both the substantial opportunities in India’s infrastructure sector and the company’s execution capabilities, while remaining mindful of valuation constraints and market risks. Regular monitoring of order wins, margin trends, and government infrastructure spending will be crucial for investment success.

The infrastructure development story in India remains compelling, and NBCC’s strategic position as a leading government contractor provides sustainable competitive advantages. However, prudent position sizing and diversification remain essential given the concentration risks and market volatility inherent in the sector.

Disclaimer:

The information provided in this article is for educational and informational purposes only and should not be considered as financial advice. Stock market investments are subject to market risks. Please consult a certified financial advisor before making any investment decisions. The author or website is not responsible for any loss incurred.